KIGALI — Rwanda’s impressive gains in financial inclusion stand in sharp contrast to emerging evidence of growing consumer risks in the country’s digital finance landscape, according to new findings.

KIGALI — Rwanda’s impressive gains in financial inclusion stand in sharp contrast to emerging evidence of growing consumer risks in the country’s digital finance landscape, according to new findings.

The findings were presented this December 9, at a workshop hosted by the National Bank of Rwanda (NBR) in collaboration with the Consultative Group to Assist the Poor (CGAP).

The workshop, convening regulators, financial institutions, fintechs, consumer advocates, and development partners, aimed to analyze the baseline assessment for Rwanda’s Responsible Digital Finance Ecosystem (RDFE) pilot.

Central to the discussions was the presentation of a nationally representative survey on consumers’ real-world experiences when using Digital Financial Services (DFS).

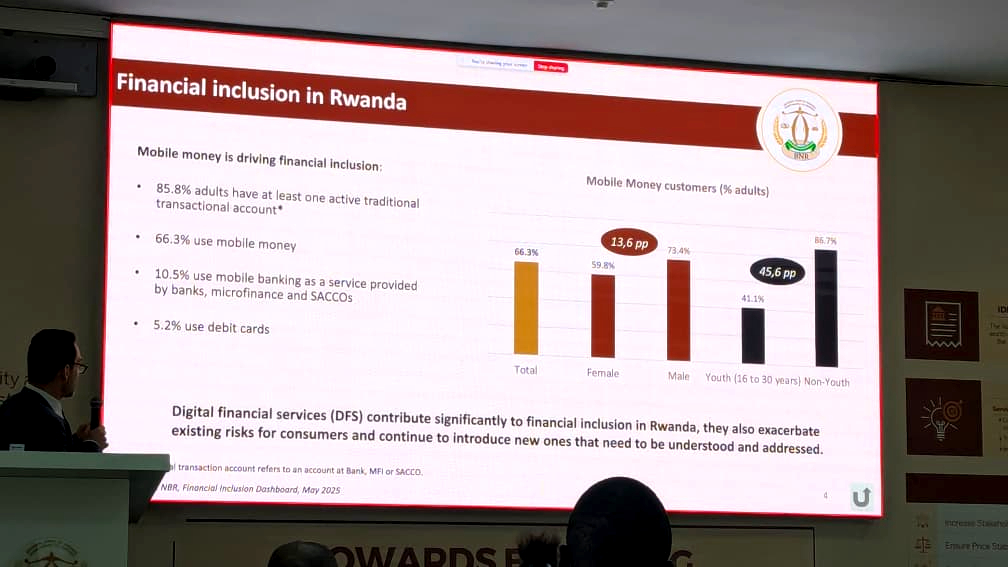

According to FinScope, Rwanda’s financial inclusion rate has reached 96%, surpassing its 2024 targets and placing the country among the region’s leaders in expanding access to financial services.

Adoption of digital financial services is also strong: FinScope reports that 73% of adults use services such as mobile money, while the NBR Financial Inclusion Dashboard indicates that 66% use mobile money, 10% use mobile banking, and 5% hold debit cards.

This expansion is seen as vital for enabling vulnerable groups—including women, low-income earners, and micro-small enterprises—to access affordable and responsible financial services that improve financial health, resilience to shocks, and economic participation.

But the new RDFE baseline assessment shows that expansion alone does not guarantee safety especially for users, and that the rapid growth of digital finance has introduced risks that are evolving faster than users can manage.

High Exposure to Fraud, Data Misuse, and Operational Failures:

The national survey, conducted in October 2025 with 1,043 DFS users, found that 97% of users experienced at least one risk linked to services such as mobile money, digital credit, and mobile banking.

Key findings include: Exposure to consumer risks where 84% experienced fraud, 65% reported agent-related risks, 48% faced transparency issues, 82% encountered capability challenges, including 41% who sent money to the wrong recipient, while 44% lost money due to risks and user-capability limitations.

The survey shows that in Digital credit, 30% of DFS users have taken digital loans but 70% faced at least one challenge, and 23% repaid late due to lack of information.

These results underscore a sharp contrast: while FinScope highlights widespread access and usage, the RDFE survey reveals deep vulnerabilities that threaten consumer trust and long-term financial health.

“This is a signial of low resilence that is why we need to come up with solutions because this has direct impact on the individual financial stability,” said Eric Duflos, CGAP’s Senior Financial Sector Specialist.

Eric Duflos

Why a New Approach:

CGAP’s global research shows that while DFS enhances inclusion, it can also amplify old risks—like fraud and poor transparency—and introduce new ones, such as data misuse, service downtime, and opaque digital credit terms.

Frank Kajungu, NBR Manager Consumer Protection Oversight emphasized that traditional consumer protection frameworks focus mainly on financial institutions, which is no longer sufficient in a digital ecosystem involving telecoms, fintechs, agents, aggregators, and third-party technology providers.

He explained the importance of the RDFE framework—developed by CGAP and currently piloted in Rwanda and Peru—highlighting that it: builds responsible practices across the whole ecosystem, strengthens governance, encourages collaboration among all actors, promotes customer-centric financial services.

“The framework goes beyond opening accounts,” he said. “We want to know how digital services are transforming livelihoods.” he said.

In a phased approach to strengthening Rwanda’s Digital Finance Ecosystem, the country is banking on the RDFE model built on three key phases:

Baseline Assessment (which was unveiled today)- National survey, role-specific self-assessments by DFS actors, and having an ecosystem mapping.

Action Planning- stakeholders jointly identify interventions to close gaps, Implementation- approved actions integrated into national plans, and a follow-up measurement every two years.

Gerald Nsabimana

Gerald Nsabimana, NBR’s Director of Financial Sector Conduct and Supervision, said the findings pave the way for policy action:

“These results enable us to move from assessment to implementation. Outcomes will inform NBR’s planning and shape future financial sector decisions so that consumers fully benefit from digital finance.”

Why the RDFE Matters:

The framework is especially important for: low-income earners, vulnerable and digitally inexperienced users, consumers who struggle with scams, complex interfaces, and network challenges.

Strengthening consumer protection—combined with improved financial literacy—is expected to boost trust, support sustainable market growth, and reinforce Rwanda’s long-term financial inclusion objectives.

Presenting the RDFE approach, CGAP’s Financial Sector Specialist Majorie Chalwe-Mulenga highlighted the need to put consumers at the center through “4 Cs” approach (Customer centricity, Commitment, Collaboration, and Capacity) needed for a responsible digital finance ecosystem.

She noted that Rwanda’s digital finance ecosystem includes: 14 consumer representatives, 150 DFS providers, 10 authorities, 35 market facilitators and 10 funders

From this landscape, 19 key actors were identified, with 12 completing detailed confidential assessments that informed the analysis.

“We need to prioritize the customer,” she stressed. “And every actor must commit resources.”

Next Steps:

Roselyn Munyana, Head of Digital Business, NCBA Rwanda explains how committed they are to deliver 99.9% of one of their digital services (MoKash)

The workshop participants agreed on the following roadmap: Draft a national RDFE action plan based on workshop findings, Validate the plan with all stakeholders, Integrate approved actions into NBR’s business plan, Coordinate with ecosystem actors for implementation, Conduct a follow-up national survey in two years to track progress and impact.

Rwanda Consumer’s Rights Protection Organization (ADECOR) official, Damien Ndizeye, called for tight measures on the ecosystem actors especially DFS’s and tech firms